The Trump Trade is Dead...all hail the Xi Trade

With all of the fuss around yesterday’s Comey testimony, I thought it would be a good time to have a look at the “Trump trades” from the beginning of the year. The charts will show that, as in the pic above, despite continued bluster and gesticulating, the “Trump Trade” has given way to the “Xi Trade”.

After the election, the big one was “Trumpflation.” The idea was that Trump is going to spend a ton of money on infrastructure and defense, leading to more bond supply, higher deficits, higher term premiums and higher inflation. This lead to an acceleration in global growth expectations, pushing inflation expectations higher around the world.

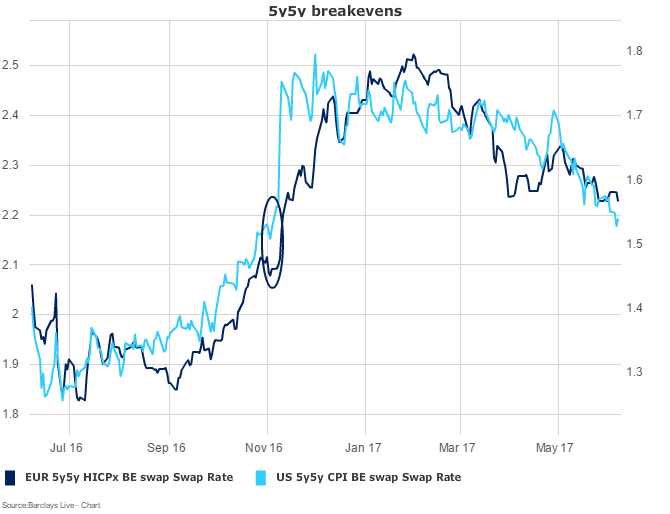

Since November, 5y5y US breakevens have been trending lower consistently. EUR 5y5y breaks took longer to reach recent highs and have been more reluctant to retrace given a better run of economic data. US breaks have retraced the whole move higher since the election, while EUR breaks are still about 10bps off those levels.

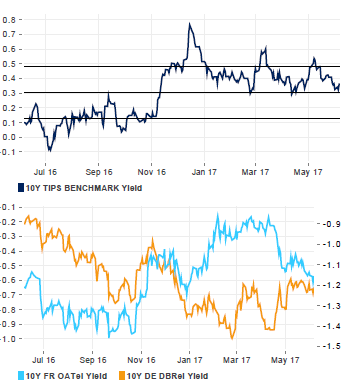

Real yields have a case of the “suppo-sta’s”. They were suppos-sta go higher.

Nominal yields have bull flattened, indicating a quick end to the Fed’s tightening cycle--not exactly a vote of confidence in Trump’s ability to increase growth rates in the US.

Not much to pick from between 10y UST (blue) and the 10y UST/Bund spread (orange).

We were also told USD would stay strong since Trump had finally solved the growth riddle, simply by promising to spend a ton of money to spur domestic demand and business investment. EUR and JPY depreciated hand-in-hand, but JPY has gone sideways while EUR has been ripping. Jens Nordvig, head of Exante Data and former Nomura FX guru, believes there has been a fundamental turn in capital flows back towards Europe. This ties out to my intuition--in 2016 capital fled Europe due to QE and low growth expectations. Now growth has picked up (a little bit, anyway), and the Trump demand resurgence has been exposed as a lot of hot air. The German export powerhouse flexes its muscle again.

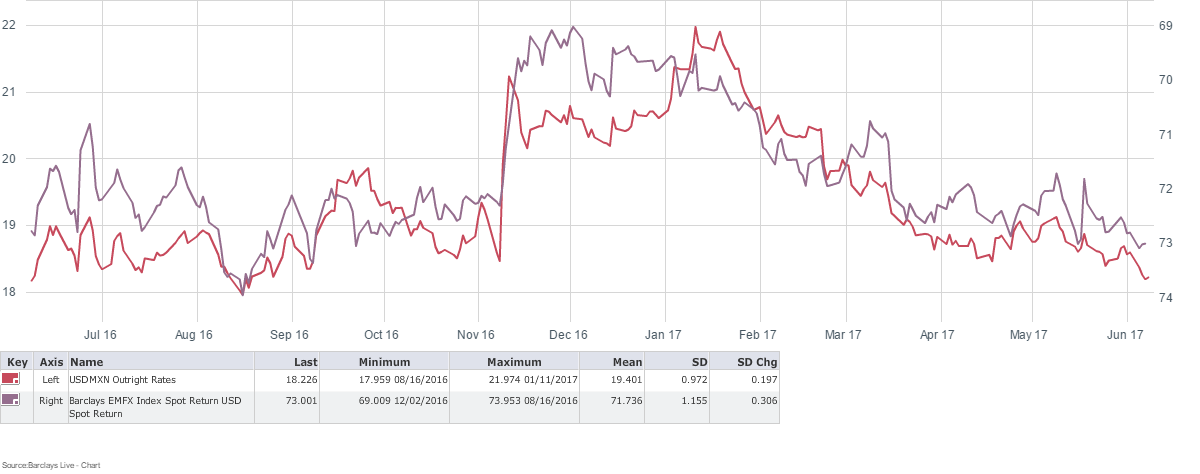

The most famous blast zone of Trump risk was usd/mxn and Mex rates. The peso fell 6% on the day after the election, and after coming back modestly into year end, melted down completely shortly after New Year’s when Trump unleashed a Twitter bomb suggesting he would implement a “border tax” on Mexican auto imports and withdraw from NAFTA. MXN moved opposite of EMFX at large, which was recovering nicely.

MXN (red) vs. EMFX (purple, inverted so it moves the same direction as MXN)

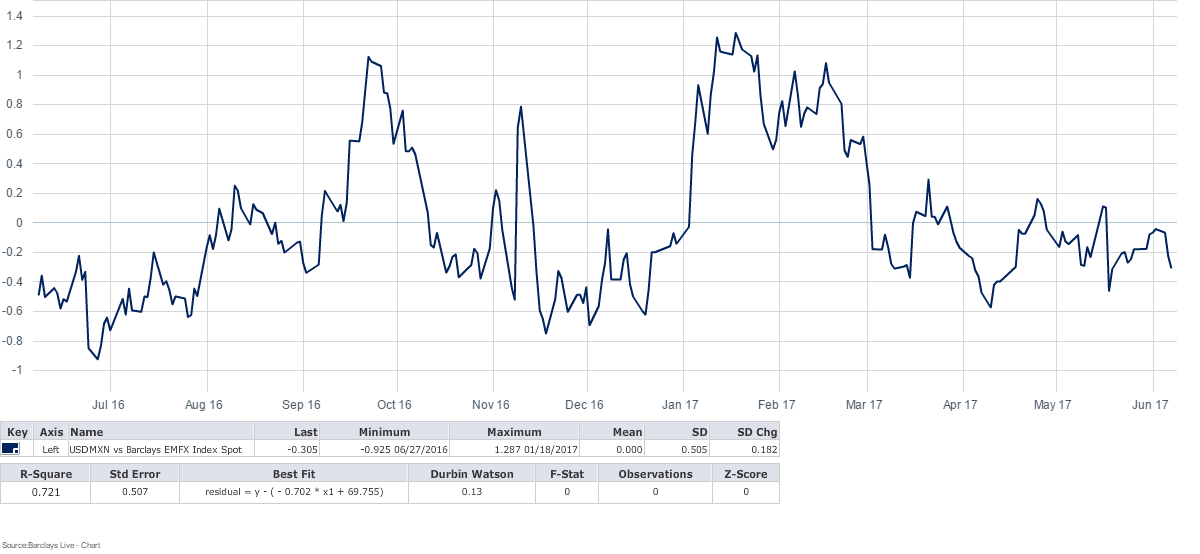

This is a chart of the residuals of usd/mxn vs. the EMFX Index--higher figures indicate MXN is cheap relative to the regression. This shows how MXN has not only closed the gap from November outright but also unwound all of the underperformance relative to the rest of EM complex.

Similarly, TIIE got demolished by Banxico aggressively hiking rates to defend the peso or financial stability, the locals' paranoia about Trump, and corporates with USD liabilities crushing offers in the cross-currency market, leaving banks as huge payers into a market with no bid.

In late February, Banxico implemented measures to backstop the peso and stabilize rates. Those measures combined with very attractive real and nominal forward rates convinced foreigners to buy duration, and local pension funds chased yields lower after moving aggressively into short duration and linkers in a futile attempt to shield themselves from the selloff in rates. These accounts extended duration as Banxico continued to hike and global curves flattened. 2x10 TIIE officially at zero….Bottom line: the herd turned.

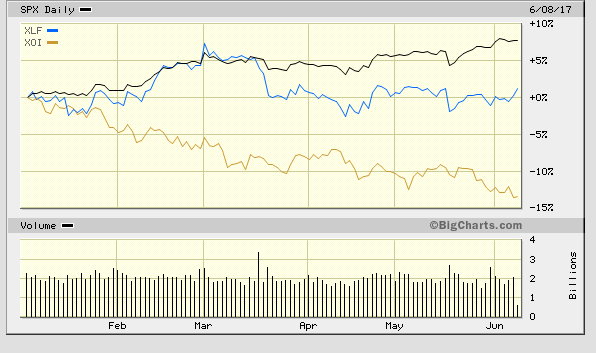

Next was stocks. “Risk on!” Came the cry from equity desks around the world. More spending! Lower corporate taxes! Offshore corporate profits repatriation! Business confidence! Deregulation! Financials and oil/gas stocks led the way, thankful that one of their own was finally back in the White House.

Since the beginning of the year financials (XLF) have chopped around while oil/gas stocks (XOI) have gotten hammered by the combo of a slothful, inept Trump administration and lower oil prices.

Similarly, small cap stocks stood strong after the election--Trump was going to cut taxes, regulate, cancel Obamacare, etc. etc. Sorry, Charlie.

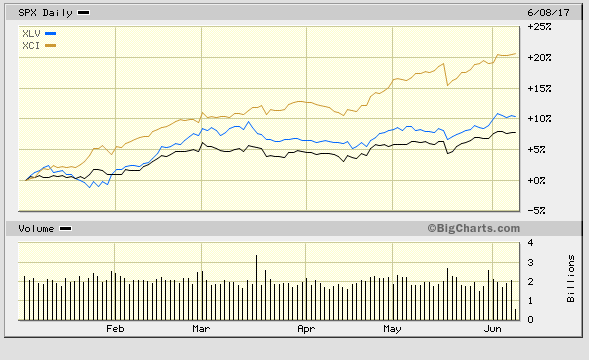

Alright, but the S&P had a great run after the election--why hasn’t it given back any of its gains? The sectors that underperformed in November and December have reversed course--Health Care (XLV), and here’s the big one--technology (XCI). The 20% gain in tech has plugged the hole in the index left by the sectors that led the big move higher late last year. Thank you, Mr. Beta.

And lastly from the equity world, there was Trump’s mantra borrowed from populist windbags the world around, “Putting America First.” A funny thing happened on the way to autarky--an avalanche of money flowed into emerging market equities.

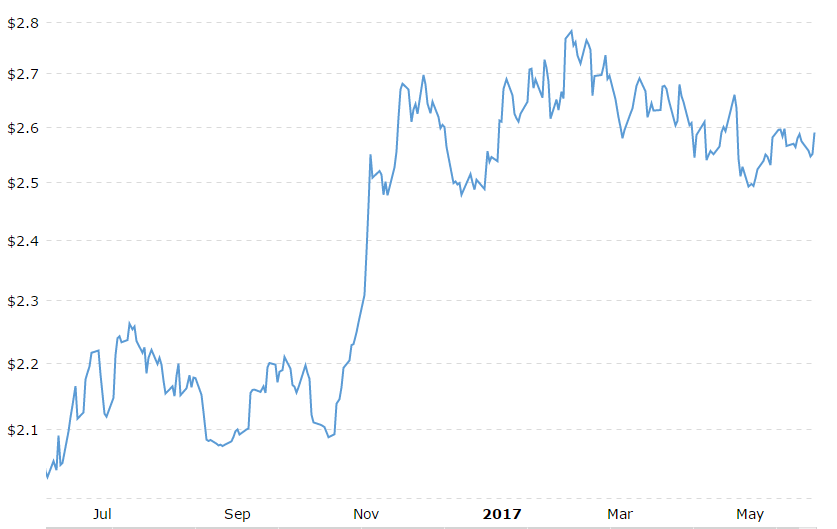

Why the reversal? Copper prices rocketed higher after the election because Trump was going to build more stuff. Here’s one that has held up, but credit goes not to Trump but to the resurgence in EM growth and Chinese demand--the Xi Trade.

Copper (HG1)

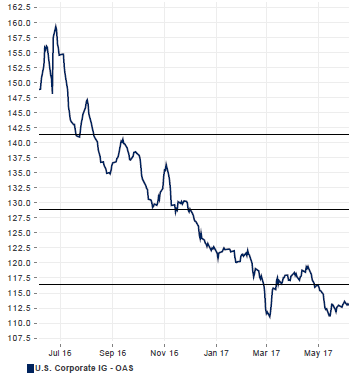

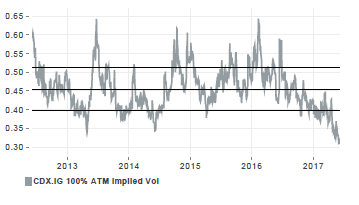

Lastly, there is credit. IG spreads were already recovering after the brutal start to 2016 and the shock from Brexit. They never really took much of a breather, just continued to grind tighter and tighter.

Vol played a significant role in this as well--was the utter destruction of vol one of his campaign promises? IG implied vol has clattered through the lows. Like tech stocks leading the S&P higher, this is credit traders juicing coupons and eating their seed corn.

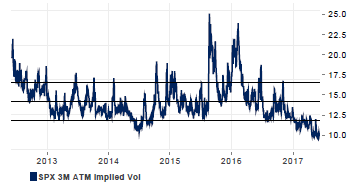

By contrast S&P vol is certainly historically low but hasn’t seen the steep decline of bond and credit vol.

Where does that leave us? I try to avoid crystal ball stuff but here’s how I see it:

-

Trump and the US political scene at large: I think he’s done politically--and taken together, the market agrees. Trump is going to be fighting with Congress, Comey and Muller until the GOP majorities get liquidated in the mid-terms. After that his agenda is over, and Democrats will be circling like sharks around a wounded tuna.

-

Nominal rates and breaks have priced fiscal stimulus at zero, which close to the right price given the way Trump has frittered away his modest political capital. But the flattening of the curve and unwinding of hikes by the FOMC beyond this year shows markets are somewhat complacent about inflation picking up on its own accord. That being said, don’t hold your breath.

-

EUR can continue to benefit from a sea change in capital flows after several years of outflows.

-

Mexico: We come here today to bury the “NAFTA withdrawal” trade. Again, if Trump could have put together a coalition of domestic manufactuers, unions, and xenophobes to rip up the treaty, he missed his chance. The TIIE curve will invert as growth stagnates and the inflation spike fades, but Banxico will be loathe to cut rates too quickly ahead of the 2018 election. Election risk will become salient around the end of the year when polls should start to become more reliable as it becomes clear who PRI and PAN will run against AMLO, but Trump’s ham-handed political circus will take some of the air out of AMLO’s campaign.

-

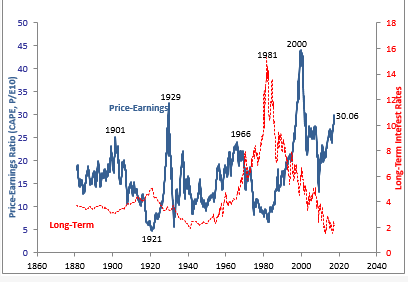

Stocks--Can’t stop the Feeling! Just dance, dance, dance…. Seriously, corporate profits will have to “show me the money” to keep this train rolling, but that hasn’t stopped the market before. This probably would have gotten me fired as an equity manager but I believe value is indicative of future returns--and I can’t see how this chart and current demographic and geopolitical trends end in a reasonable return on risk capital, unless 1929, 1966, and 2000 were really good times to buy stocks.

-

IG, HG, vol--see above. Taken together, real money is getting squeezed and is increasing risk by buying tech, high yield, selling vol etc. to keep the ball rolling. The longer it goes on, the smaller the exit door gets.

-

EUR, DXY, EM--the prior two bullets notwithstanding, I think the flows can keep going--I prefer EM rates over EMFX--but I’ll want the hedges I discussed in Wednesday’s post in my back pocket. The resilient copper chart illustrates global demand is still stronger than it was last year. This is the new paradigm for 2017….the Xi Trade.

Comments

Post a Comment